PLEASE NOTE: To qualify for the EV charger tax credits, the charger must be operational by June 30, 2026.

EV Charging Incentives Webinar – Jan. 15, 2026

The Alternative Fuel Vehicle Refueling Property Tax Credit (30C) – let’s just call it the EV charging tax credit – was reauthorized by Congress in the 2022 Inflation Reduction Act (IRA). The law changed some of the details about eligibility and amounts and, until recently, the details have been a bit fuzzy. In September 2024, the IRS published proposed guidance on eligibility and brought this tax credit into focus, allowing about two-thirds of Americans to receive tax credits on EV charging infrastructure.

The 30C EV charging tax credit offers up to 30% off the cost of installing EV chargers for individuals for personal use, for businesses, and for tax-exempt entities. You heard me right. How does a tax-exempt entity get a tax credit? Well, this tax credit offers a direct pay option for tax-exempt entities which allows nonprofit organizations, municipalities, schools, churches, and charities the ability to install chargers and file for the tax credit as if they paid taxes. They can then receive a rebate from the IRS for installing the chargers or the seller of the charging equipment can claim the credit and pass that amount on to the tax-exempt entity.

I want to install an EV charger for:

Why does this federal EV charging tax credit matter?

Plug In America’s EV Driver Survey (and many other consumer surveys) shows that one of the most significant barriers to EV adoption is the lack of access to EV charging. These tax credits address this barrier by making EV charging installations more affordable while creating jobs, lowering transportation costs, strengthening energy security, and reducing vehicle pollution.

Location qualification: Here is what you need to know

In order to qualify for the Federal EV Charging Tax Credit, the equipment must be installed in a low-income census tract or a non-urban census tract, regardless of whether it is for use by an individual, a business, or a tax-exempt entity. To determine whether your charging site is located in an eligible census tract, you can look up the location.

- Check your eligibility through the Refueling Infrastructure Tax Credit Mapping Tool:

- Go to this website: https://experience.arcgis.com/experience/3f67d5e82dc64d1589714d5499196d4f/page/Page

- Enter your address into the search tool in the upper-right-hand corner.

- The “Tract Status” legend (to the left of the map) will show the eligibility of your census tract.

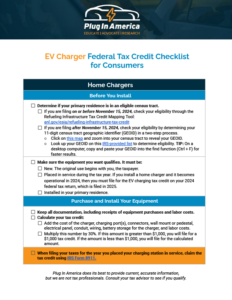

EV charger tax credit for personal use

If you purchase and install (or have installed) an EV charger for personal use, the tax credit is up to 30% of the cost of the charger and installation – up to $1,000 – per single item of property.

If you purchase and install (or have installed) an EV charger for personal use, the tax credit is up to 30% of the cost of the charger and installation – up to $1,000 – per single item of property.- A single item of property is the system used to charge one EV at a time at the rated electrical output. This includes one or more charging ports, the charger, connector, wall mount or pedestal, new electric panel, conduit, wiring, and battery storage at the point where the vehicle is charged.

- Equipment must be new.

- You must file for the tax credit for the year the charging infrastructure was placed in service. For example, if you install a home charger and it becomes operational in 2024, then you must file for the EV charging tax credit on your 2024 federal tax return.

- The EV charging equipment must be installed at your primary residence.

- The residence must be in an eligible low-income community or non-urban census tract. See location qualification section above.

Download the consumer checklist

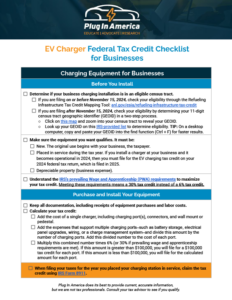

EV charger tax credit for a business

- I

f you purchase and install (or have installed) an EV charger for business use, the tax credit is up to 6% of the cost of the charger(s) and installation – up to $100,000 – per single item of property.

f you purchase and install (or have installed) an EV charger for business use, the tax credit is up to 6% of the cost of the charger(s) and installation – up to $100,000 – per single item of property. - If the project meets prevailing wage and apprenticeship requirements, the project is eligible for a 5X multiplier and the tax credit is up to 30% of the charger(s) and installation cost – up to $100,000 – per single item of property.

- A single item of property is the system used to charge one EV at the rated electrical output at a time. This includes one or more charging ports, the charger, connector, wall mount or pedestal, electric panel, conduit, wiring, charge management system, and battery storage at the point where the vehicles are charged.

- For installations of multiple charging ports, expenses that support multiple charging ports—such as battery storage, electrical panel upgrades, wiring, or a charge management system—will be allocated across the number of charging ports.

- Equipment must be new.

- Businesses must file for the tax credit for the year it was placed in service. For example, if you start installation in 2024 but the chargers are not operational until 2025, then you would file for the tax credit on your business’s 2025 federal tax return.

- The EV charging equipment must be depreciable property and used for business purposes.

- The EV charging installation must be in an eligible low-income community or non-urban census tract. See location qualification section above.

Download the business checklist

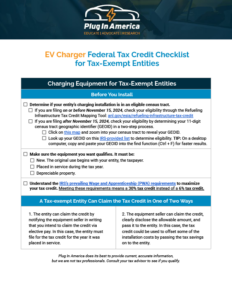

EV charger tax credit for a tax-exempt entity

If you purchase and install (or have installed) an EV charger for your entity’s use, the tax credit is up to 6% of the cost of the charger(s) and installation—up to $100,000—per single item of property.

If you purchase and install (or have installed) an EV charger for your entity’s use, the tax credit is up to 6% of the cost of the charger(s) and installation—up to $100,000—per single item of property.- If the project meets prevailing wage and apprenticeship requirements, the project is eligible for a 5X multiplier and the tax credit is up to 30% of the charger and installation cost – up to $100,000 – per single item of property.

- A single item of property is the system used to charge one EV at the rated electrical output at a time. This includes one or more charging ports, the charger, connector, wall mount or pedestal, electric panel, conduit, wiring, charge management system, and battery storage at the point where the vehicles are charged.

- For installations of multiple charging ports, expenses that support multiple charging ports—such as battery storage, electrical panel upgrades, wiring, or a charge management system—will be allocated across the number of charging ports.

- Equipment must be new.

- Tax-exempt entities can access the tax credit in two ways:

- The entity can claim the credit by notifying the equipment seller in writing that you intend to claim the credit via elective pay. In this case, the entity must file for the tax credit for the year it was placed in service.

- The seller can claim the credit, clearly disclose the allowable amount of the credit, and pass it along to the entity. The credit can be used to offset installation costs.

- The EV charging equipment must be depreciable property.

- The EV charging installation must be in an eligible low-income community or non-urban census tract. See location qualification section above.

Download the Tax-exempt entity checklist

Plug In America does its best to provide current, accurate information, but we are not tax professionals. Consult your tax advisor to see if you qualify for tax credits.