Important: The guidance on this page is for vehicles delivered on or after January 1, 2023. For guidance on EV tax credits between Aug. 17, 2022 and Dec. 31, 2022, visit our summary here.

This page was last updated on March 10, 2023.

The MSRP caps changed on Feb. 3, so please review the section on EVs that qualify and check the IRS page for the latest MSRP caps.

On Dec. 29, 2022 the U.S. Department of Treasury and Internal Revenue Service released further guidance on the Clean Vehicle Tax Credit that is part of the Inflation Reduction Act (IRA). The IRA is a significant investment in clean energy and transportation technologies and includes an array of electric vehicle (EV) incentives. Our experts share the things you need to know.

Just a reminder that we offer this information as our best interpretation of the IRS guidance and we do not guarantee what we’ve shared will ensure a consumer will be eligible for any tax benefit. We recommend that you consult a tax advisor or legal counsel, as well as check the IRS website for the most up-to-date information.

Table of Contents

- EV Tax Credit Changes for 2023

- Webinar

- New EV Tax Credit Requirements

- EVs That Qualify for the 2023 Tax Credit

- Frequently Asked Questions for New EVs

- Used EV Tax Credit Requirements

- Frequently Asked Questions for Used EVs

- More Information

EV Tax Credit Changes for 2023

Starting January 1, 2023, the most significant changes to Clean Vehicle Tax Credit are:

- New clean vehicles are eligible for up to $7,500 depending on battery size until further guidance from the Treasury/ IRS is released in March 2023.

- Previously owned clean vehicles (also known as “used vehicles”) are eligible for a tax credit of up to $4,000.

- The minimum battery capacity must be 7 kilowatt hours

- Vehicles must be made by a qualified manufacturer

- MSRP limitations apply

- Income limits apply to taxpayers

- The taxpayer must report the vehicle identification number (VIN) of the vehicle on the taxpayer’s income tax return

- Dealers must provide reports to the taxpayer and the IRS regarding the sale of the vehicle

Webinar

On Jan. 12, we hosted a webinar to review the most recent IRS guidance, as well as answer questions. A recording of the webinar is available to watch on YouTube, and you can also download the slides on Slideshare.

Correction: We mistakenly answered the question about income limits as being the greater of income from 2022 and 2023. The correct answer is that the income limits are the lesser of income from 2022 and 2023. Apologies for the oversight! See more in our FAQs.

New Clean Vehicle Tax Credit Requirements

| Vehicle | Buyer |

|

|

EVs That Qualify for the Clean Vehicle Tax Credit

The following models qualify for the clean vehicle tax credit under the Treasury and IRS interim guidance if you take delivery on or after Jan. 1, 2023 but before the Treasury and IRS rulemaking is released in March. However, different trim levels of the same model have different MSRP limits, so consumers should cross-reference the IRS page as well as consult a tax professional or attorney.

Let’s explain MSRP first. It stands for “manufacturer’s suggested retail price.” For the purposes of this tax credit , the MSRP is the base retail price of the vehicle plus the price of any optional equipment physically attached to the vehicle at the time of delivery to the dealer. It does not include destination charges or optional items added by the dealer, or taxes and fees.

The reason consumers need to check the IRS page and consult tax professionals is that some variations of the same model have different MSRPs. For example, the Tesla Model Y 7-seat variations have a sales price limit of $80,000 while the 5-seat variations have a cap of $55,000. Since the Model Y 5-seat variations have a starting price that is currently more than the $55,000 cap, these vehicles are not eligible for the $7,500 tax credit. At this time, we are not clear what criteria the IRS is using to qualify vehicles as SUVs, vans and pickup trucks vs. other vehicles. We will continue to update this page as we get clarity surrounding this guidance.

Update on March 10, 2023: The Department of Energy has created a list of qualifying vehicles with their MSRP caps.

Frequently Asked Questions for New EVs

1. How much is the tax credit?

The tax credit can be up to $7,500 depending on battery size. The base amount is $2,500 plus $417 per each additional kilowatt hour (kWh) in excess of 5kWh. The vehicle must have at least 7 kWh of battery that can be charged from an external source (be able to be plugged in). The minimum credit amount (if a vehicle only has a 7 kWh battery) is $3,751 ($2,500 + 3 * $417). This means that vehicles with at least 12 kWh of battery will get the full credit. This currently includes all fully electric vehicles and many, but not all, plug-in hybrids.

2. What about battery components and critical mineral sourcing requirements?

The Treasury will conduct a rulemaking to determine guidance on battery sourcing requirements beginning in March of 2023. Once this guidance is released, the new guidance will take effect. For vehicles delivered before the guidance is released, the sourcing requirements do not apply.

3. What time period does the information on this page cover?

The guidance provided for the new clean vehicle tax credit that was released on Dec. 29, 2022 applies between Jan.1, 2023 and when the preliminary guidance on the battery sourcing requirements is released by the Treasury Department and the I.R.S., which is expected in March 2023.

4. Does this guidance apply to when I ordered the vehicle or when I received it?

The guidance applies to the time period when you receive your vehicle, not when you order it or put a deposit on it. For example, if you ordered your EV in 2022 and you pick it up in February of 2023, this guidance will apply. However, if you order your vehicle in January 2023 and it arrives in July of 2023 and the next round of guidance has been released by the I.R.S. The tax credit will be subject to the updated guidance, not the guidance discussed on this page that was released on Dec. 29, 2022.

5. Which year are the income limits for?

Purchaser income limits begin on January 1, 2023 and continue to be a requirement for the New Clean Vehicle Tax Credit (technically known as 30D), as well as the Used Clean Vehicle Tax Credit (technically known as 25E) through the end of 2032. If you purchase a vehicle in 2023, in order to qualify for the tax credit, either your Modified Adjusted Gross Income (MAGI) for that taxable year (2023) or the preceding year (2022) must be below the threshold amount.

6. What if you expect your income to be different in 2023 than 2022?

Assuming you are planning to purchase an EV in 2023, you will qualify based on the Modified Adjusted Gross Income (MAGI) that is the lesser of the two.

An example: You are a single filer and had a MAGI of $145,000 in 2022 but expect to make $155,000 in 2023. The single filer limit is $150,000. Your MAGI for 2022 is the lower of the two years, and that is what you will use to determine if your income qualifies. Since you have a MAGI of $145,000 below the $150,000 threshold, your income qualifies for the tax credit.

7. Are the income limits talking about gross income or something else?

The income limits are based on Modified Adjusted Gross Income. According to the IRS, your modified AGI is the amount from line 11 of your Form 1040 plus:

- Any amount on line 45 or line 50 of Form 2555, Foreign Earned Income.

- Any amount excluded from gross income because it was received from sources in Puerto Rico or American Samoa.

8. If I am leasing an EV and at the end of my lease I purchase the vehicle from the dealer, will the used vehicle purchase tax credit apply?

We are still researching this. We have reached out to our federal contacts on this and are waiting for a response. We will be sure to share the answer as soon as we receive additional guidance.

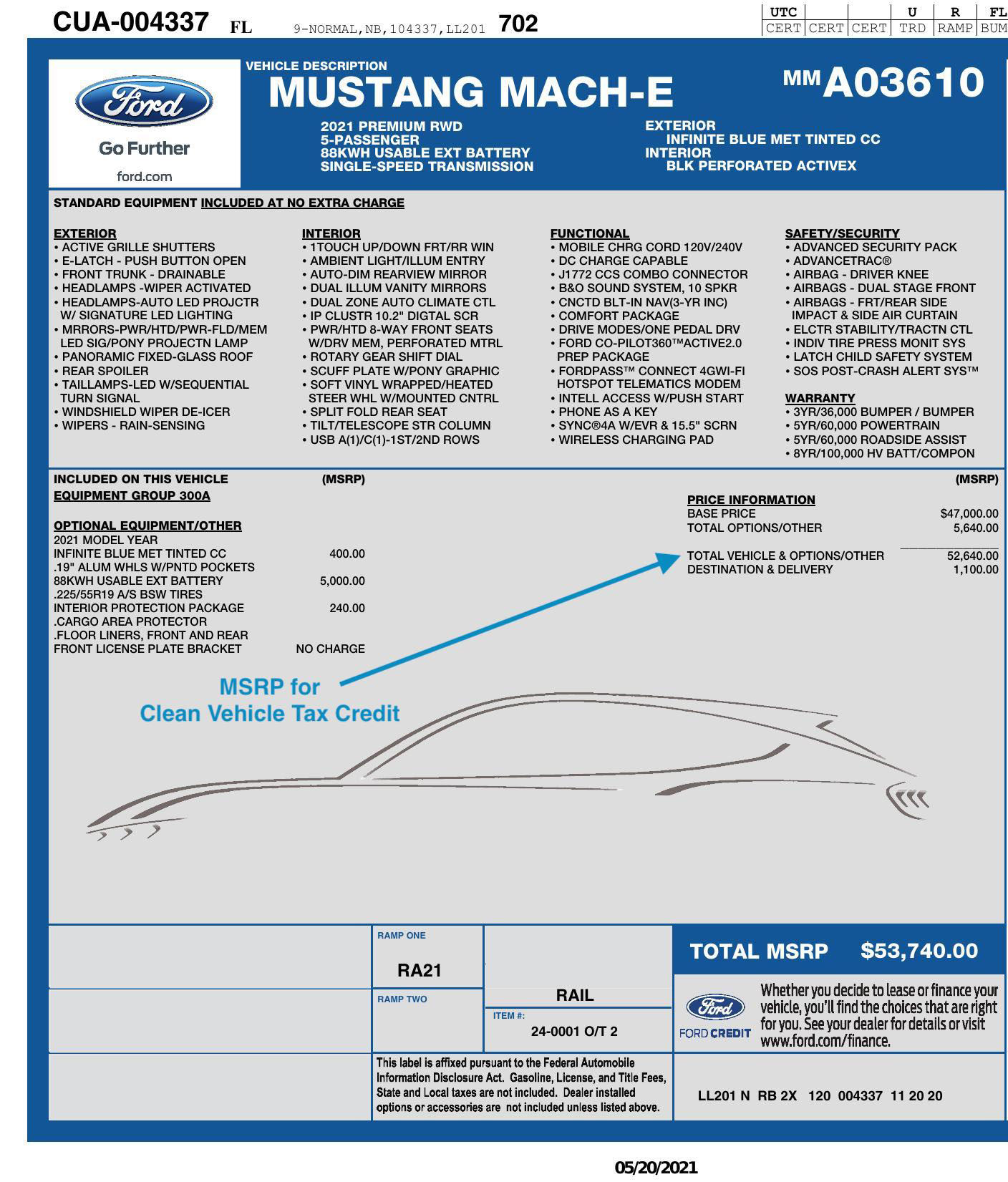

9. How do I determine if the vehicle I want meets the MSRP cap?

The MSRP is the base retail price suggested by the manufacturer, plus the retail price suggested by the manufacturer for each accessory or item of optional equipment physically attached to the vehicle at the time of delivery to the dealer. It does not include destination charges, optional items added by the dealer, or taxes and fees. The MSRP caps are as follows:

- Vans / SUVs / Pickup Trucks – $80,000

- Other – $55,000

If the vehicle arrives at the dealer and the MSRP on the sticker is below the cap for that vehicle, it should be eligible for the tax credit as long as the other Clean Vehicle Tax Credit requirements are met.

To help consumers understand where to look on stickers, the MSRP in this case would be $52,640 for tax credit purposes.

10. How do I know whether my vehicle will be defined as a truck, van, SUV or other type of vehicle for the purposes of the MSRP cap?

The Treasury Index to Manufacturers identifies the applicable MSRP limit, so if you look up the vehicle you are interested in under the manufacturer, the model will indicate the MSRP limit.

11. What is a Qualified Manufacturer?

A qualified manufacturer is a manufacturer that enters into a written agreement with the IRS. A list of qualified manufacturers is maintained by the IRS and can be found here.

12. Can I get the tax credit by leasing a new clean vehicle?

If you lease a vehicle, the lessor (company that maintains the vehicle title) is the original user. This means that they will claim and receive the tax credit, but they can pass it along to the lessee (you) in your lease payments.

13. Are vehicles made by manufacturers that have sold over 200,000 vehicles eligible for the tax credit in 2023?

They are. As of Jan.1, 2023 the prior sales volume limits no longer apply. This means GM vehicles and Tesla vehicles are eligible for the tax credits.

14. If I ordered a vehicle in 2022 and it is delivered in 2023, do the income limits and MSRP limits apply?

Yes, the tax credit guidance is based on when the vehicle is placed in service, so if you take delivery of your vehicle in 2023, the guidance beginning Jan. 1, 2023 applies. We do not know which vehicles will be eligible for the credit once the rules on battery components and critical minerals are released in March. The rules are expected to be complex and it is possible that few or no vehicles will be eligible then. Thus, if you are intending to buy a vehicle that is currently eligible for the credit, it may make sense for you to move quickly to try to take delivery before the new rules are released in March.

15. If I order a vehicle in January of 2023, but it doesn’t arrive until after the Treasury issues guidance on the battery component and critical mineral requirements, will it be eligible for the tax credit?

It depends on the guidance from the Treasury Department and whether the vehicle meets the critical mineral and battery component requirements at that time. The Treasury Department guidance on critical mineral and battery component requirements will take effect the day after it is issued from the Treasury Department.

16. Can non-taxable entities like cities or counties get the commercial tax credit?

Yes, the Commercial Clean Vehicle Tax Credit (also known as 45W) is refundable (or direct pay) for tax-exempt entities like cities or counties. This means that tax-exempt entities can claim and receive the tax credit even though they don’t pay any taxes. The I.R.S. treats the tax credit as if it was an overpayment of taxes and refunds the money to the tax-exempt entity even though no taxes were paid.

Used Clean Vehicle Tax Credit Requirements

| Vehicle | Buyer |

|

|

Frequently Asked Questions for Used EVs

1. How much is the tax credit?

The previously-owned clean vehicle tax credit can be up to $4,000 or 30% of the vehicle sales price, whichever is less.

2. Can businesses receive the previously-owned clean vehicle tax credit?

No, only individuals can receive the previously-owned clean vehicle tax credit.

3. Do I have to purchase the vehicle from a dealer?

Yes, to be eligible for the tax credit, the vehicle must be purchased from a dealer.

4. If a vehicle has already received a tax credit when it was purchased as new, is it eligible for the used tax credit?

Yes. A vehicle is limited to one credit per vehicle for each type of credit meaning that a vehicle can receive the tax credit as a new vehicle and again as a used vehicle for a different owner.

5. Does the vehicle purchase price for the previously-owned clean vehicle tax credit depend on the type of vehicle purchased, such as a van, pickup truck, SUV or other vehicle?

No, all previously-owned clean vehicles are eligible for a tax credit of up to $4,000 or 30% of the vehicle sales price, whichever is less.

More Information

This guidance is from FS-2022-42, published December 29, 2022.

Additional guidance can be found through the Department of the Treasury’s press release here: https://home.treasury.gov/news/press-releases/jy1179

Other resources:

- List of Manufacturers and Models for New Qualified Clean Vehicles (Internal Revenue Service)

- VIN decoder for vehicle build location information (Department of Energy)

Disclaimer: Plug In America offers this information as our best interpretation of the IRS guidance and does not guarantee its accuracy or that what we have shared will ensure a consumer will be eligible for any tax benefit. We recommend that you consult a tax advisor or legal counsel.